Why I’m Rating Chevron a Buy

- Felix Ouma

- 3 days ago

- 8 min read

Summary

As Chevron enters 2026, it boasts record production levels, an enhanced upstream portfolio, and a balance sheet that allows for continued investment and shareholder returns.

The key narrative extends beyond oil prices, encompassing a combination of cash flow from the Permian Basin, growth in the Gulf of America, the Tengiz expansion, Hess synergies, and prudent capital expenditure.

Despite recent successes, Chevron remains appealing compared to Exxon Mobil and ConocoPhillips when considering valuation alongside portfolio quality, dividend reliability, and disciplined cash returns.

The primary risk continues to be commodity prices. If oil prices, refining margins, or project execution fall short, the stock may stagnate, although the business is now more robust than it was a few years ago.

Investment Thesis

I believe Chevron (NYSE: CVX) is a BUY. The simple reason is that the company is now in a stronger position than the headline earnings numbers alone suggest. In 2025, Chevron delivered record production, integrated Hess, started up major projects, kept capital spending under control, and still returned a record amount of cash to shareholders. During the fourth-quarter 2025 earnings call, management described 2025 as “a year of execution,” and that feels like the right starting point for the thesis. This is not a turnaround story built on hope. It is a large, high quality energy company that has already done much of the hard work and is now moving into the cash-harvest phase of several big projects.

What makes Chevron attractive to me is that the company now has multiple engines working at the same time. The Permian has reached scale and is shifting from volume growth toward free cash flow growth. Tengiz has moved from a long construction story into a producing asset. The Gulf of America is adding new barrels from projects that are already online. The Hess acquisition added Guyana and Bakken exposure, and management says integration is largely complete. On top of that, Chevron continues to run a disciplined downstream business that helps smooth some of the volatility that always comes with oil prices. When I look at that mix, I see a business that is better balanced, more durable, and more cash-generative than the market may be giving it credit for.

The other thing I like is the company’s mindset. Chevron is not promising explosive change every quarter. It is talking about production growth, cost reductions, strong shareholder returns, and steady capital allocation. That tends to be exactly what works best in a cyclical industry. In the 2025 Annual Report, the company said it stands in the strongest position management has seen in years, with lower execution risk and a clearer line of sight to future cash flow. That confidence matters because a lot of Chevron’s heavy lifting is no longer in front of it. Much of it is now already operating.

Business Overview

Chevron is one of the largest integrated energy companies in the world. That matters because this is not just an oil producer. It has upstream assets, refining and chemicals operations, trading exposure, and a growing set of new energy businesses. In the 2025 Annual Report, Chevron described itself as an integrated energy company with a premier upstream portfolio, a resilient downstream and chemicals business, and a focused lower-carbon portfolio. For regular investors, the practical takeaway is simple: the company has more than one way to make money.

The upstream side is the main value driver. In 2025, Chevron produced 3.7 Mn barrels of oil-equivalent per day, up 12% from 2024. The company also ended the year with about 10.6 Bn barrels of proved reserves. Record production was helped by the Hess acquisition, Permian growth, Tengiz ramp-up, and the Gulf of America. That gives Chevron both scale and depth. It also gives the company a better spread of assets across shale, conventional offshore, LNG, and international production.

The downstream side still matters too. Chevron delivered its highest U.S. refinery throughput in two decades, which shows that this is not just a pure commodity-price bet. When refining and chemicals are running well, they can support cash flow even when upstream pricing is less favorable. That kind of diversification is one reason Chevron often deserves a quality premium versus a more concentrated producer.

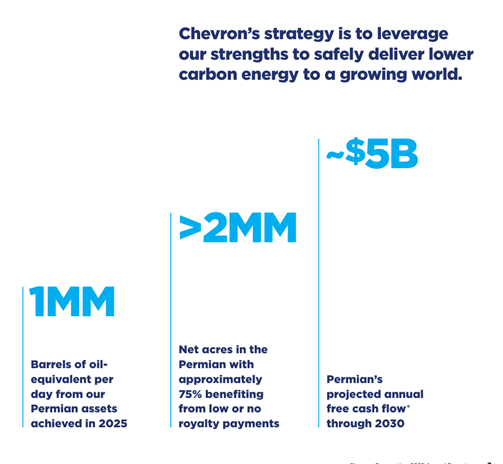

Portfolio strength in one image

Chevron’s Permian strategy is now more about cash generation than chasing volume. The chart below from the 2025 Annual Report highlights the scale of the asset and why it matters to the investment case.

Chevron's Growth Drivers

The first big driver is the Permian. In the 2025 Annual Report, Chevron said Permian production averaged 1 Mn barrels of oil-equivalent per day in 2025, a target it had introduced more than five years ago and delivered on schedule. More importantly, the company now says its Permian strategy has shifted from rapid growth to disciplined value delivery. That is exactly what I want to hear. Once a shale position reaches scale, the real question becomes how much cash it can throw off, not how many more barrels can be added. Chevron’s annual report says the Permian is expected to generate about $5 Bn of annual free cash flow at mid-cycle prices. That is a major part of the bull case all by itself.

The second driver is project ramp-up outside shale. During the fourth-quarter 2025 earnings call, management pointed to the Future Growth Project at Tengiz, start-ups at Ballymore and Whale, and the ramp-up of Anchor in the Gulf of America. These are not vague future ideas. They are real projects that are either already online or very close to full contribution. Chevron also said Gulf of America production is advancing toward 300 thousand barrels of oil-equivalent per day in 2026. That matters because offshore barrels tend to be long-life and high-margin when projects are executed well.

The third driver is Hess. This is not just about adding volume. It is about adding quality barrels and long-duration growth. In the annual report, Chevron said integration is largely complete and that it is on track to achieve $1.5 Bn of synergies. It also highlighted the Guyana Stabroek Block, where the acquisition gives Chevron a 30% stake in one of the most attractive growth assets in the industry. That improves the long-term portfolio in a meaningful way.

The fourth driver is cost discipline. In the February 2026 investor presentation and the fourth-quarter materials, Chevron said it delivered $1.5 Bn of structural cost savings in 2025 and remains on track for a $3 Bn to $4 Bn run-rate reduction by the end of 2026. Cost programs are easy to dismiss when they are just targets. They become more important when management has already started delivering them. In Chevron’s case, the early progress supports the idea that future cash flow can improve even without a major move higher in oil prices.

The fifth driver is shareholder returns. Chevron increased its quarterly dividend by 4% to $1.78 per share and bought back $12.1 Bn of stock in 2025, plus Hess shares acquired at a discount. The company’s message is clear: cash flow growth is meant to show up in investor returns. In a sector where discipline often comes and goes, that consistency matters.

Valuation

Using valuation multiples, Chevron trades at a FWD EV/EBITDA of 7.13x, a FWD P/E of 15.01x, and a FWD PEG of 0.58x. Exxon Mobil (NYSE: XOM) trades at 7.68x EV/EBITDA, 14.51x P/E, and 0.75x PEG. ConocoPhillips (NYSE: COP) trades at 5.65x EV/EBITDA, 14.68x P/E, and 0.93x PEG.

At first glance, Chevron does not look “cheap” on every single line. ConocoPhillips is lower on EV/EBITDA, and Exxon is slightly lower on FWD P/E. But that is exactly why the full picture matters. Chevron’s PEG of 0.58x is the lowest in the group, which tells me the stock still looks attractive relative to expected growth. In plain English, the market is not charging much extra for the amount of growth and cash-flow improvement that may still be ahead.

I also think Chevron deserves to be judged on quality, not just on the lowest multiple in the peer set. Compared with Exxon, Chevron looks a little cheaper on EV/EBITDA and materially cheaper on PEG, while still offering a similar large-cap, integrated, shareholder-return story. Compared with ConocoPhillips, Chevron is more expensive on EV/EBITDA, but Conoco is a more concentrated upstream name. Chevron gives investors a broader platform, more downstream balance, a long dividend track record, and multiple project-driven cash flow levers beyond just commodity exposure.

So why is Chevron still a good option? Because the valuation is reasonable for what the company is becoming. You are not paying a stretched multiple for a speculative story. You are paying a fair multiple for a business with record production, visible project ramp-up, improving cost structure, a stronger post-Hess portfolio, and a shareholder-return policy that is already being funded. In my view, that combination is enough to support a Buy rating even in a sector where headline valuations can look similar at first glance.

Key Risks

The clearest risk is oil price weakness. Chevron is still an energy company, so if Brent falls sharply and stays low, earnings and cash flow will feel it. Management’s own sensitivity documents make that clear. The business is stronger than before, but it is not immune to commodity prices.

The second risk is execution risk around big projects and integration. Chevron has already made strong progress, but projects like Tengiz, offshore ramp-ups, and the full value capture from Hess still need to keep delivering. Large projects can be delayed, cost more than expected, or underperform early.

The third risk is downstream and chemicals weakness. Chevron’s integrated model is a strength, but it also means weaker refining margins or chemicals earnings can hold back results, as management noted in the fourth-quarter 2025 materials.

The fourth risk is geopolitical and regulatory exposure. Venezuela, Kazakhstan, Guyana, and global LNG all create opportunity, but they also bring political and policy risk. Chevron is used to operating in these environments, but investors should still respect that exposure.

Final Thoughts

Chevron looks like a Buy to me because the company is entering 2026 with stronger assets, better momentum, and more visible cash generation than it had a few years ago. The Permian is now a cash machine, not just a growth story. Major projects are moving from build-out to contribution. Hess has improved the portfolio. Cost savings are showing up. And investors are still getting meaningful dividends and buybacks along the way.

This is not the cheapest stock in the energy sector on every metric, and it does not need to be. What matters is that Chevron still looks reasonably valued for the quality of the business, the durability of the portfolio, and the amount of cash it should be able to generate if management executes as expected. For me, that is enough to keep the stock in Buy territory.

Introducing the alpha Brief Portfolio (aBP)

We’re also excited to share some news on our side. We’ve launched the alpha Brief Portfolio, a concise, research‑driven collection of ideas built for thoughtful investors who want signal without the noise. The goal is simple. We aim to surface well‑researched names for long‑term compounding, with clear theses, entry ranges, risk factors, and realistic holding horizons. It will read like a briefing you can act on, not a doorstop report that gathers dust. We’ll weave it into these Friday recaps so you can follow the thinking in real time, and we’ll keep the tone neutral and disciplined because process beats hot takes over a full cycle.

If you’re looking for solid, research-backed stock ideas with real growth potential, check out the alpha Brief Portfolio. It focuses on companies that fit a GARP (Growth at a Reasonable Price) theme, combining data-driven selection with sound fundamentals using our in-house Quant Models. You can follow every move we make, see the companies we’re tracking, and stay aligned with our strategy.

Important Disclosure

Past performance is no guarantee of future results. Therefore, you should not assume that the future performance of any specific investment or investment strategy will be profitable or equal to corresponding past performance levels. Inherent in any investment is the potential for loss. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Henriot Investment Management Ltd is not a fiduciary by virtue of any person’s use of or access to the Site. Henriot Investment Management is not a licensed securities dealer, broker or investment adviser or investment bank.

Comments